Today’s Mortgage Rates (APR)

| Program | Today’s APR* | Yesterday’s APR | Trend |

| 30 Year Fixed | 3.76% | 3.73% | +.03% |

| 15 year Fixed | 3.07% | 3.05% | +.02% |

| 5/1 Hybrid ARM | 2.96% | 2.93% | +.03% |

Commentary — Mortgage Rates Continue Last Week’s Upward Trend

Data are mixed this morning but weighted toward increasing rates. All three major stock indexes are up, as are oil prices. These point to a heating economy, which is bate for interest rates. However, the benchmark ten-year Treasury rate has backed off by two basis points (two 100th of one percent) to 1.74 percent. Anything below two percent is considered quite low.

No News Today; Rates Up Slightly

There are no pertinent economic reports today, so expect mortgage interest rates to be primarily influenced by stock prices and global news. This is typical for a Monday. Right now, stocks are up, and they’re pulling rates along. If you’re floating an interest rate, keep an eye on the news and stay in contact with your mortgage lender. There will be a lot going on this week, culminating in Friday’s Monthly Employment Report for February.

Tomorrow

Tomorrow bring s fairly important report; the Institute for Supply Management’s (ISM) manufacturing index for February. It measures the strength of the manufacturing sector as interpreted by manufacturers. That’s a big deal and it can really shake things up if it varies much from analysts’ expectations.

Experts anticipate that it increased from January’s 48.2 to 48.7 in February. That’s still considered pessimistic — any reading below 50.0 means the majority of surveyed manufacturers felt business declined during the month. If the actual report shows high-than-expected optimism, it could cause mortgage rates to increase; the reverse is also true.

Recommendation

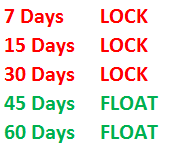

Rates are low, today’s indicators point to an increase in the near future, and if I were financing a house today, I’d be inclined to lock. If 45 or 60 day locks could be had for less than .25 discount points, I’d be inclined to lock for a longer term as well. Your own tolerance for risk may vary — this is just what I would do.

Here we go:

TUTORIAL: How Do Bond Prices Affect Interest Rates?

Bonds are issued in $1,000 amounts and each bond has what’s called a “coupon rate,” which determines the interest payment that its owner receives. For example, if you purchase a $1,000 bond with a five percent coupon rate, you’ll get $50 in interest every year. ($50 interest / $1,000 price = .05, or 5.0 percent.) If you can buy a $1,000 bond for $1,000, its price is called “par.” However, movements in financial markets cause bond prices to change all the time. Suppose the markets crash, and interest rates drop to three percent. Everyone would want a five percent bond in that case, so its price would go up. If the $1,000 bond goes for $1,200, its owner still gets $50 a year interest. However, he or she has paid more than par for the bond, so its yield (rate) is no longer five percent. $50 interest / $1,200 price = .0417, or 4.17 percent. And if inflation kicks in and investors only want yields of at least eight percent? $50 interest / .08 = $625. To get an 8.0 percent yield, then, investors won’t pay more than $625 for the bond. Prices will fall and yields will rise. The charts below show this relationship.